In India, companies can issue a variety of investment instruments to investors to meet their capital requirements. Under Indian company law, such instruments issued to investors are called ‘securities’. Depending on a company’s financial needs and investor preferences, several fundraising options are available for consideration.

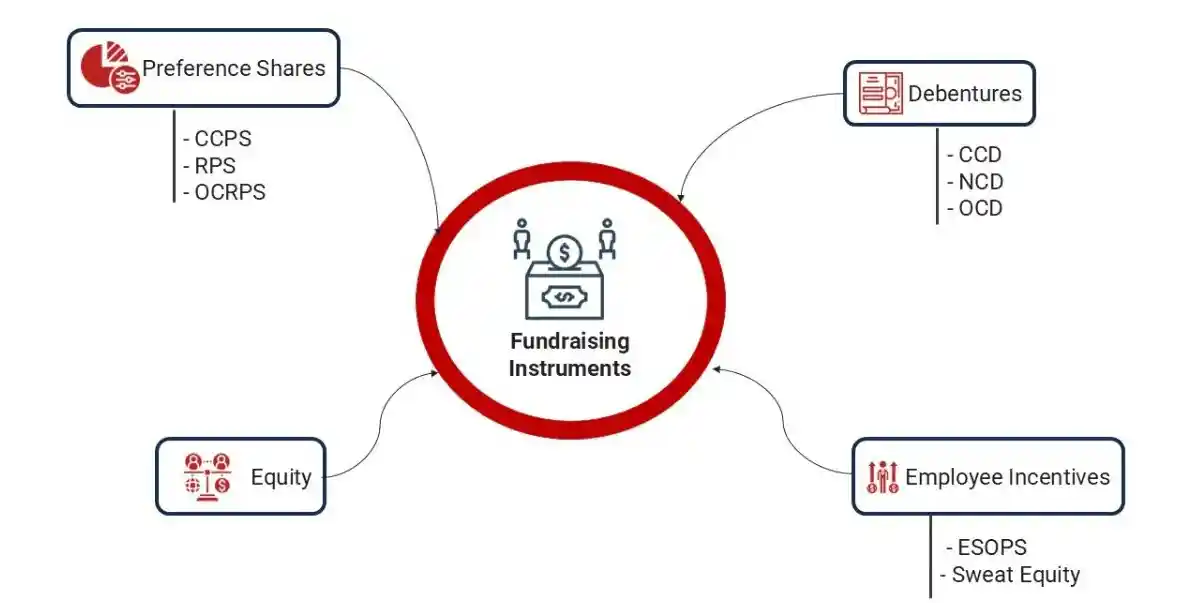

Fundraising Instruments:

At the time of raising capital, companies commonly issue equity instruments, debt instruments, or hybrid instruments that combine the features of both debt and equity.

The key difference between issuing equity and debt instruments lies in whether the shareholding of existing investors becomes diluted.

Types of Fundraising Instruments:

Equity:

Companies can raise funds through equity financing without creating debt, allowing investors to hold a share of the ownership of the company

CCPS (Compulsory Convertible Preference Shares):

Compulsory Convertible Preference Shares operate as hybrid or anti-dilution instruments, combining fixed dividends with the potential for conversion into equity. Conversion of the instrument may depend on the performance of the company, which benefits investors by allowing flexibility in conversion of the instrument. If targets are not specified, the company can increase its stake.

RPS (Redeemable Preference Shares):

Redeemable Preference Shares have a fixed tenure and allow companies to raise temporary capital, giving flexibility in financial planning.

OCRPS (Optional Convertible Redeemable Preference Shares):

Optional Convertible Redeemable Preference Shares provide flexibility by allowing conversion into equity or repayment based on mutual agreement. This structure benefits both investors and companies by aligning with performance or shared preferences.

CCD (Compulsorily Convertible Debentures):

CCDs, like Compulsorily Convertible Debentures, are hybrid instruments that convert into equity within a specified period. Until conversion, they function as debt, providing companies with structured fundraising opportunities.

NCD (Non-Convertible Debentures):

Non-Convertible Debentures are debt instruments preferred by investors seeking fixed returns. They include interest and principal repayment but do not convert into equity.

OCD (Optionally Convertible Debentures):

Optionally Convertible Debentures allow debentures to be converted into equity or repaid under agreed terms. This structure offers flexibility while combining elements of debt financing.

Employees Stock Option Plans (ESOPs):

Employees Stock Option Plan grant employees the right to purchase company shares at a pre-determined price on a predetermined date. Companies use ESOPs as tools to attract and retain skilled employees, while also aligning employee interests with company success.

Sweat Equity Shares:

Companies issue sweat equity shares to founders, directors, or employees at discounted prices or for non-cash consideration, recognising their contributions. By issuing such shares, companies retain and reward employees for their services.

Compliances for Issuance of the Financial Instruments:

Companies may issue equity shares to existing shareholders through rights issuance after securing board approval. Following approval, offer letters must be sent to shareholders detailing the rights issue period. The board resolution also needs to be filed with the Registrar of Companies. Once funds are received, the board approves the allotment of the equity shares to the shareholders, and the return of allotment must be filed by the company with the Registrar of Companies. Funds received from the right issue cannot be used until the share allotment takes place and the return is filed with the Registrar.

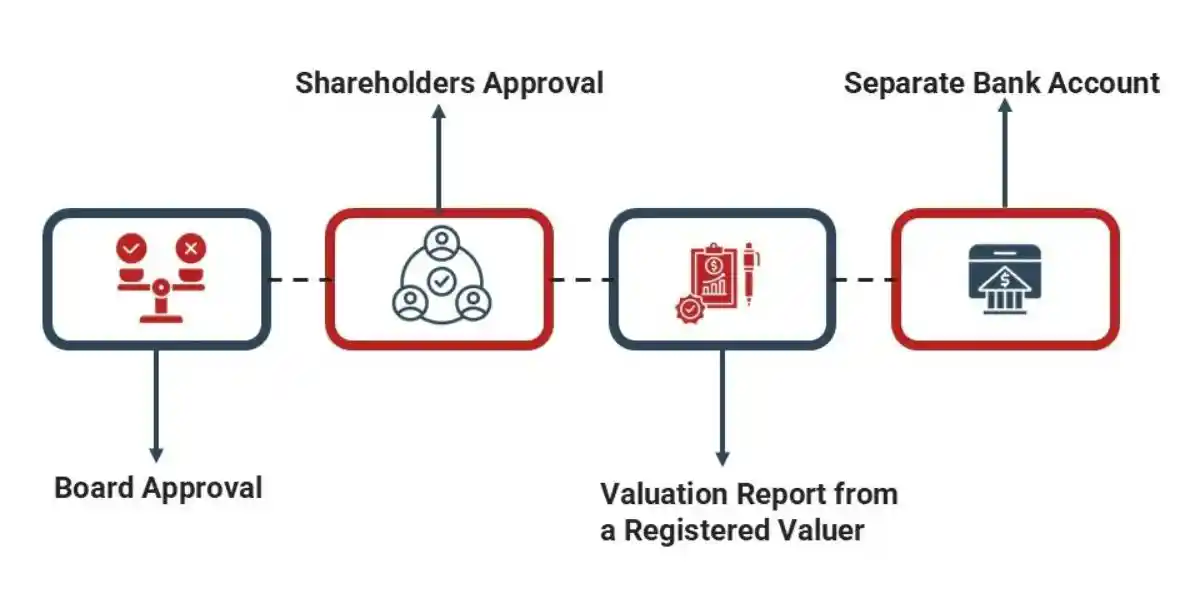

For preferential offers made to new investors, the process involves:

- Obtaining a valuation report from a registered valuer.

- Gaining approval from the board of directors for the preferential issue.

- Securing shareholder approval through a special resolution.

- Opening a separate bank account where investors remit funds.

- Filing the special resolution with the Registrar of Companies.

- Sending offer letters to investors.

- Allotting shares once funds are received, and filing the return of allotment.

- Utilising funds only after the return of allotment is filed.

- If equity or preference shares are issued, corporate actions must be filed with depository participants to credit instruments to investor demat accounts. For CCDs or OCDs, share certificates may be issued.

For ESOPs, the compliance process includes:

- Board approval for issuing ESOPs.

- Shareholder approval through a special resolution.

- Filing the resolution with the Registrar of Companies.

- Updating the Register of Employee Stock Options.

- Granting options to employees.

- Vesting and subsequent exercise of options.

- Allotting shares once options are exercised and filing the return of allotment.

- Filing corporate actions with depositories for crediting instruments to investor demat accounts.

- Including necessary disclosures in the board’s report.

For Sweat Equity Shares, the process requires:

- Obtaining a valuation report from a registered valuer.

- Securing board approval.

- Securing shareholder approval through a special resolution.

- Filing the resolution with the Registrar of Companies.

- Allotting shares after approval and filing the return of allotment.

- Recording entries in the Register of Sweat Equity Shares.

- Making disclosures in the board’s report during the year of issue.

For Non-Convertible Debentures, companies may issue only secured NCDs. If unsecured NCDs are issued, listing on a recognised stock exchange becomes mandatory to prevent classification as deposits.

For secured Non-Convertible Debentures, the company must ensure:

- Redemption does not exceed 10 years, except in infrastructure-related sectors where redemption can extend to 30 years.

- NCDs are secured by creating a charge equal to the value of repayment of principal and interest.

- Appointment of a debenture trustee with defined roles and qualifications.

- Creation of a Debenture Redemption Reserve (DRR) by 30th April. This reserve must equal 15% of debentures maturing in the following financial year. The amount may be invested in scheduled banks or government securities and used only for redemption.

If instruments are issued to non-resident investors, FEMA compliance becomes mandatory. Companies must check sectoral caps, acquisition rules, and pricing guidelines. Once met, companies must file Form FC-GPR within 30 days of issuing instruments to non-residents.

Subscription of Non-Convertible Debentures by foreign investors other than FPIs is treated as External Commercial Borrowing (ECB) under FEMA rules.

External Commercial Borrowings (ECB):

Indian entities can raise ECBs as commercial loans in foreign currency from non-resident lenders. ECBs are allowed only for defined periods, known as the Minimum Average Maturity Period.

Key Takeaway for Preference/Equity/OCD/CCD/Sweat Equity

For the rights issuance of equity shares, board approval alone is required.

Conclusion:

The complexity of financial instruments makes customised strategies essential for effective capital raising and ownership management. To handle this complexity with precision, seeking professional guidance is critical.

Why Choose India Company Incorpration (ICI)?

Our team at India Company Incorporation property of InCorp has extensive experience in raising funds through various instruments. To learn more about our services and how we assist with fundraising, contact us at (+91 77380 66622 or email us at info@incorpadvisory.in