For accounting and taxation purposes, a transfer price emerges when related parties, such as company divisions or a company and its subsidiary, need to report their individual profits. A transfer price is utilised to determine costs when these related parties are required to conduct transactions with each other. Generally, transfer prices do not vary significantly from market prices.

A transfer price is a price that represents the value of goods or services exchanged between independently operating organisational units. Transfer pricing, on the other hand, refers to transaction prices between associated enterprises that may occur under conditions different from those between independent enterprises.

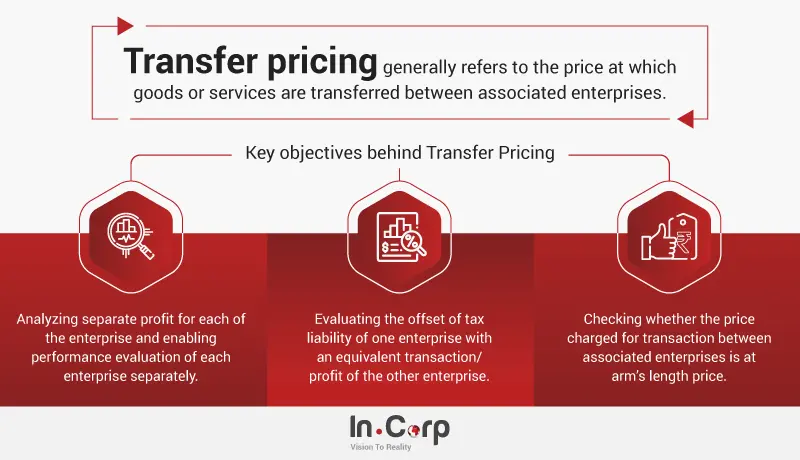

Transfer pricing typically refers to the price at which associated enterprises transfer goods or services. Such transactions can encompass product sales, service provision, money lending, and the use of (intangible) assets. Consequently, transfer pricing effects result in the parent company or a specific subsidiary generating insufficient taxable income or excessive transaction losses. For example, setting high transfer prices can increase profits accruing to the parent by siphoning profits from subsidiaries in high-tax countries, while low transfer prices can move profits to subsidiaries in lower-tax jurisdictions.

In simple terms, the prices and conditions set between related parties under transfer pricing policies should align with those that would be agreed upon between independent, unrelated companies.

What is the objective of Transfer Pricing?

An Associated Enterprise is an enterprise that participates in, or in respect of one or more persons who participate, directly or indirectly, or through one or more intermediaries, in the management, control, or capital of the other enterprise.

Arm’s Length Price refers to the price that should have been charged between related parties had those parties not been related to each other.

Constituent Entity can be defined as the following:

- Any entity of the international group that is included in consolidated financial statements for financial

reporting purposes or included if the equity share of any entity of the group were to be listed. - Or any entity of the group that is excluded from consolidated financial statements based on size or materiality.

- Or any permanent establishment of an entity of the group if separate financial statements are prepared for

financial reporting, regulatory, tax reporting, or internal management control purposes.

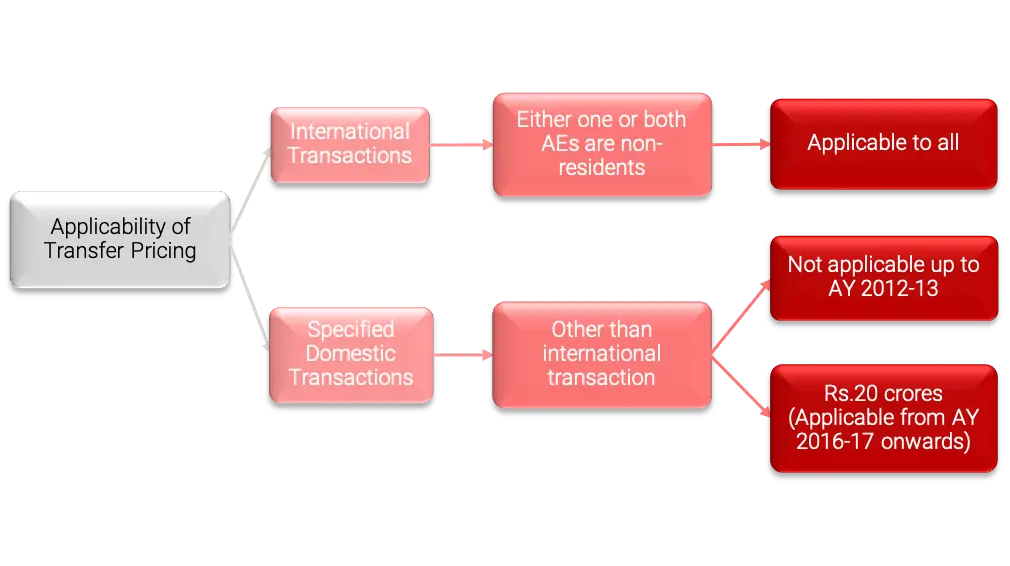

Part 1: Applicability and Scope of Transfer Pricing

1. Which transactions are subject to transfer pricing regulations?

2. Which transactions are covered under transfer pricing?

The following transactions are covered under Transfer Pricing:

| International Transactions | Specified Domestic Transactions |

|---|---|

| • Provision of software development services

• IT services • Knowledge process outsourcing services • Provision of intragroup loans • Provision of corporate guarantees • Manufacture and export of auto components • Receipt of low-value intragroup services • Provision of contract R&D services relating to software development or generic pharmaceutical drugs |

• Supply of electricity

• Transmission of electricity • Wheeling of electricity • Purchase of milk or milk products by a co-operative society from its members |

3. What are the various types of deemed Associated Enterprise (AE)?

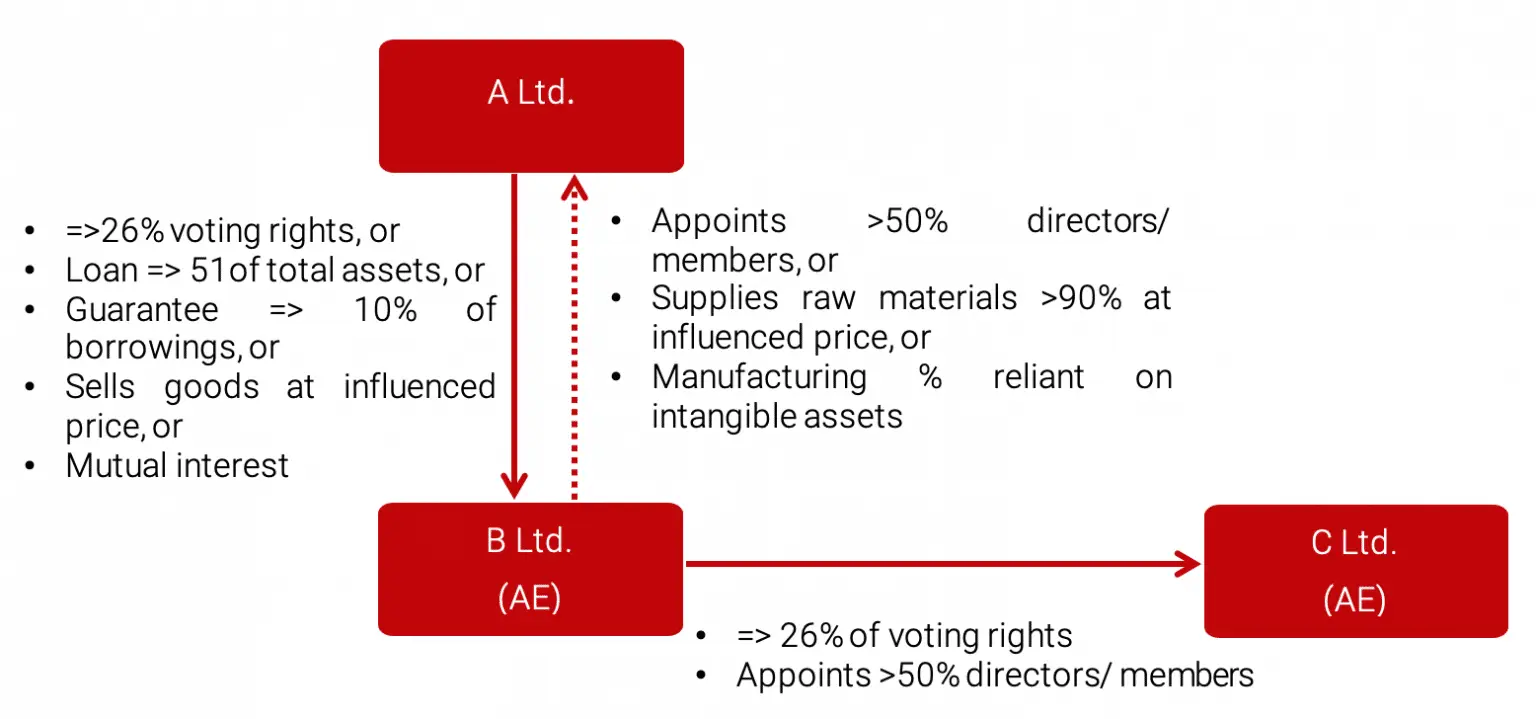

In the case of A Ltd., the following entities will be associated enterprises if:

- A Ltd. holds ≥ 26% voting power in B Ltd. Further, B Ltd. holds ≥ 26% voting power in C Ltd.

- A Ltd. provides a loan to B Ltd. ≥ 51% of the book value of the total assets of B Ltd.

- A Ltd. guarantees ≥ 10% of the total borrowings of B Ltd.

- B Ltd. appoints > 50% of directors/members of the governing board or one or more executive directors of A Ltd.

- Further, C Ltd. appoints > 50% of directors/members of the governing board or one or more executive directors

of B Ltd. - Manufacturing of goods of A Ltd. is wholly reliant on intangible assets of B Ltd.

- B Ltd. supplies > 90% of raw materials to A Ltd. for manufacturing, where the price is influenced by B Ltd.

- A Ltd. sells goods to B Ltd. at the price decided by B Ltd.

- A Ltd. and B Ltd have a mutual interest.

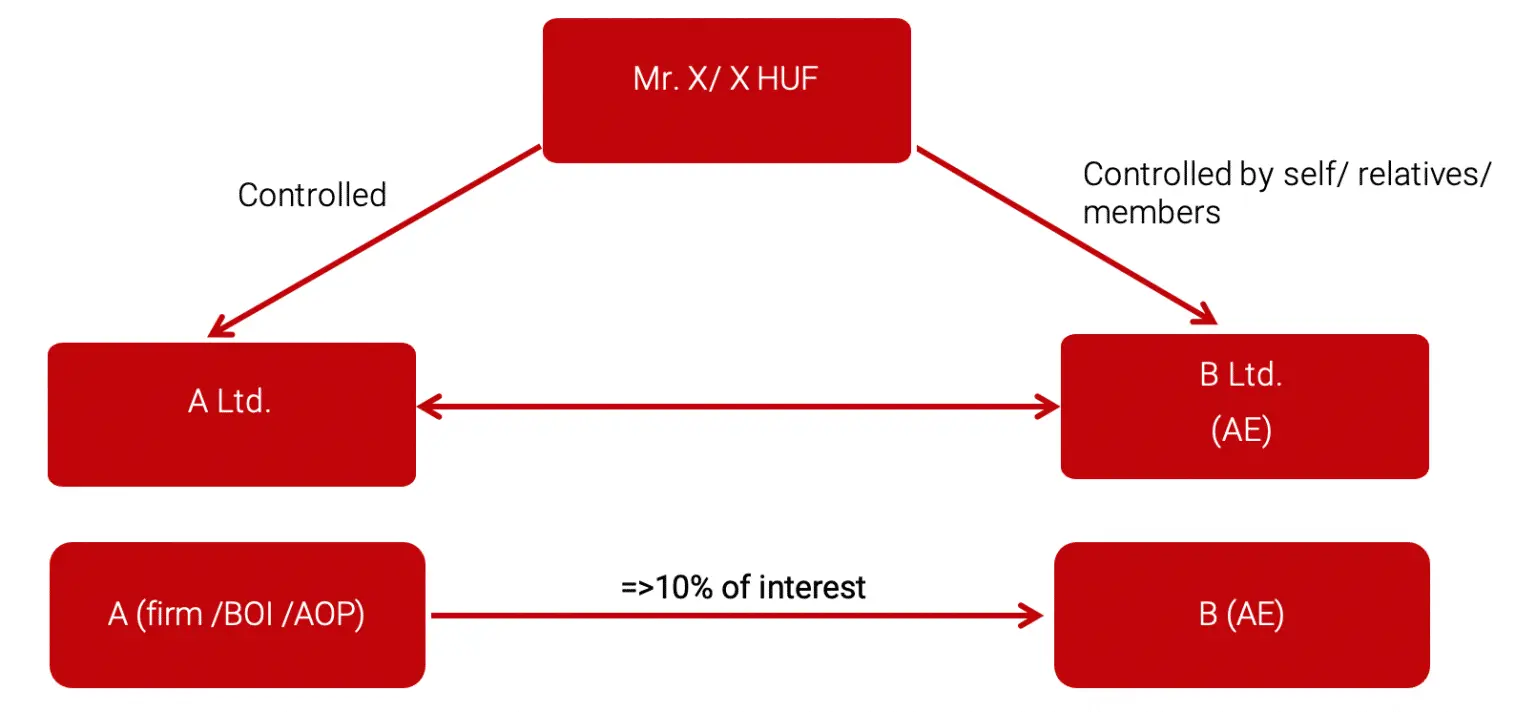

- A Ltd. is controlled by Mr. X/HUF and B Ltd. is controlled by Mr. X/HUF or relatives of Mr. X/HUF.

For example,

Part 2: Methods for Computing Arm’s Length Price

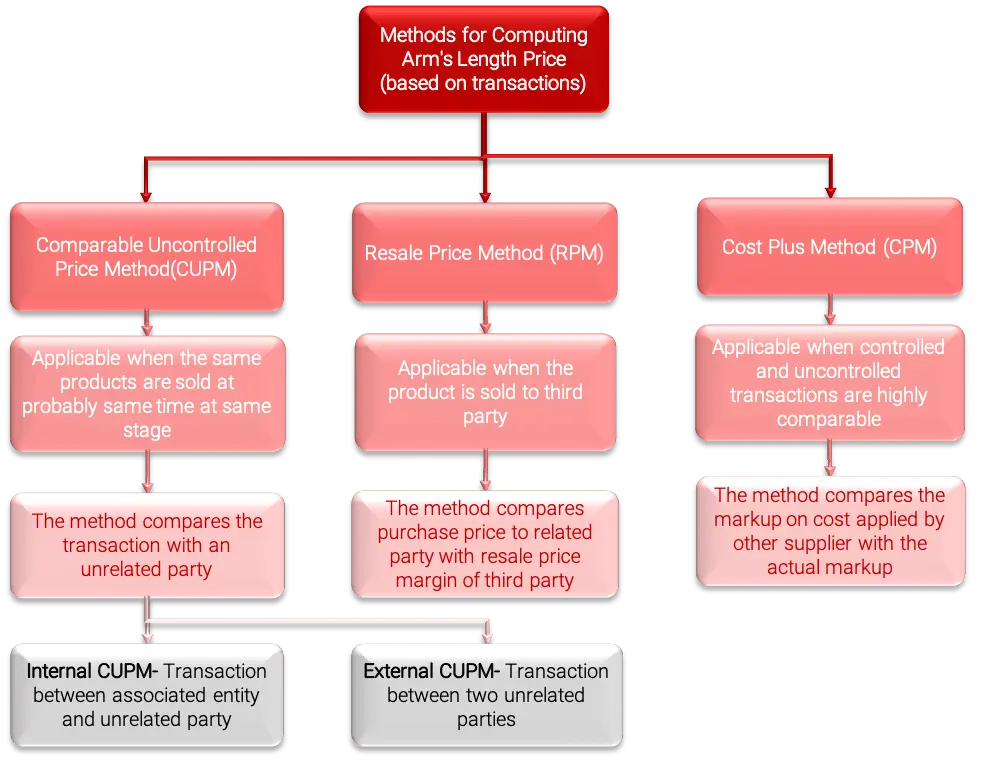

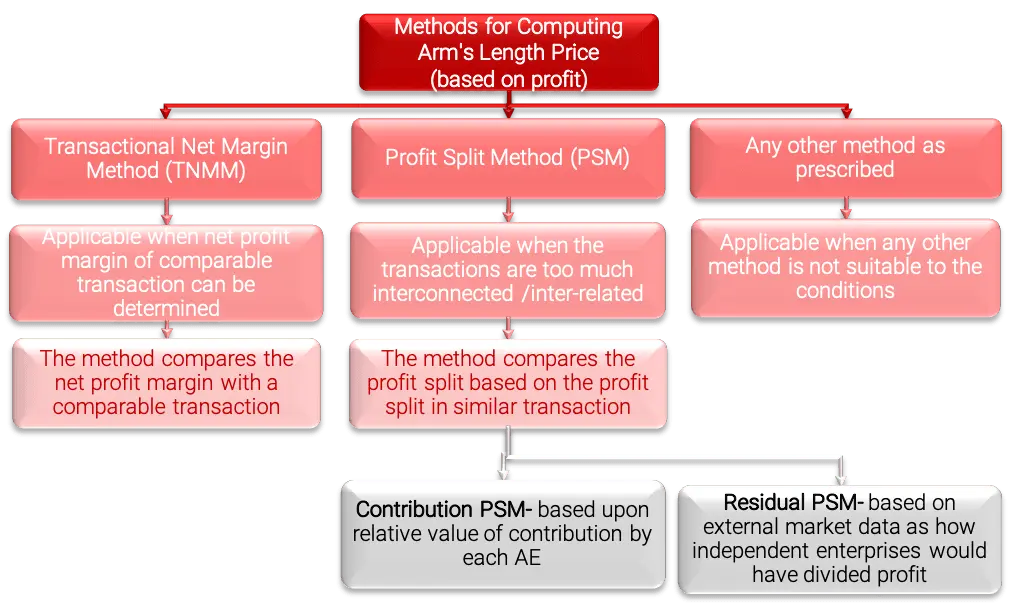

1. What are the methods to compute the Arm’s Length Price?

The various methods for computing the Arm’s Length Price are as follows:

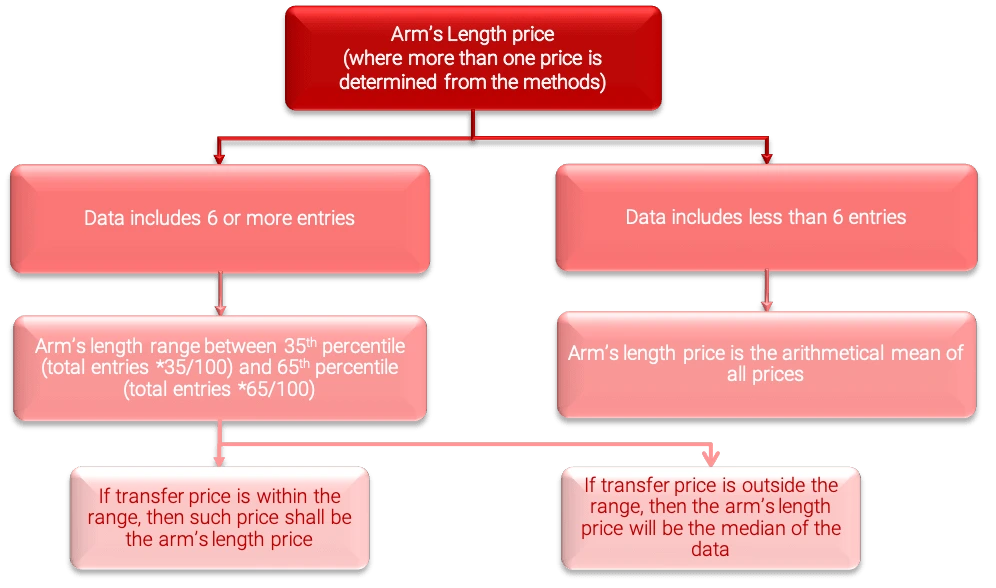

2. What will be the ALP when more than one price is determined from the methods?

Note: If the variation of arm’s length price does not exceed 1% in case of wholesale trading and 3% in

other cases, such transfer price will be deemed to be arm’s length price as per Rule 10CA of Income Tax Rules.

Wholesale trading refers to the transaction of trading in goods where the purchase cost is 80% or more of the total cost

and the average monthly closing inventory is 10% or less of the sale of such goods.

Part 3: Documentation and Compliance

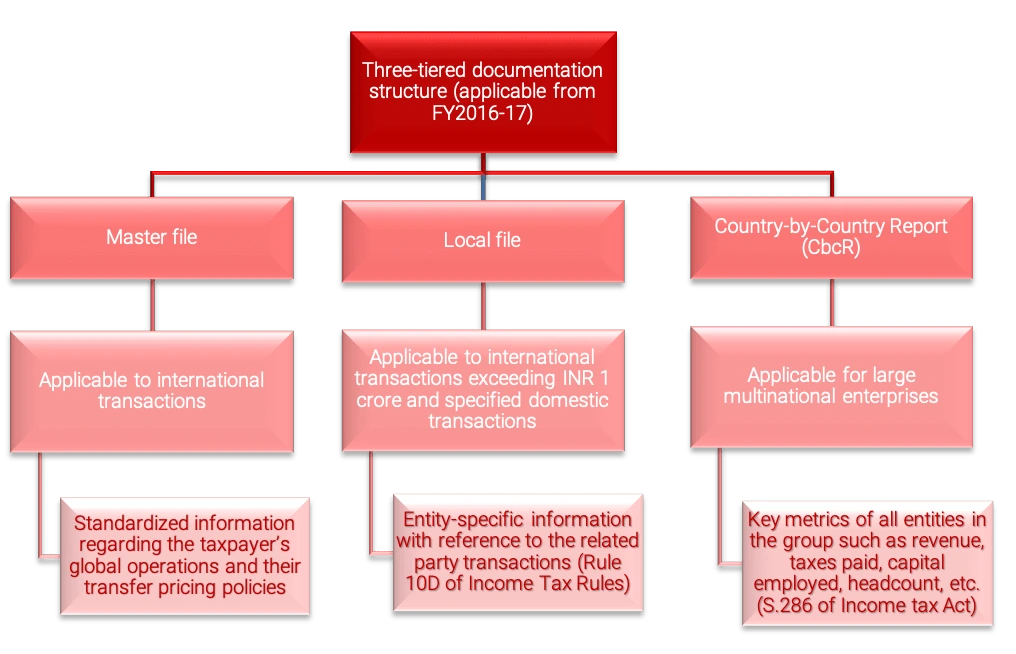

1. What is the documentation structure under transfer pricing?

2. What are the documents required to be maintained?

Information and documents to be maintained as per Rule 10D of Income Tax Rules

| Basic Documents | Supporting Documents |

|---|---|

| • Details of ownership structure of the enterprise

• Profile of the group in which the enterprise is a part • Business overview of the taxpayer and associated enterprises • Details of the transaction (name of the associated enterprise, nature, terms, quantity, value) • Description of functions performed, risk assumed, assets employed • Record of relevant financial forecasts/ estimates made, economic analysis and budgets • Details of the uncontrolled transaction (nature, terms, conditions, analysis to evaluate comparability) • Details of the method selected for determining the arm’s length price • Record of actual working, assumptions, policies for determining arm’s length price • Details of adjustments, if any, made to the transfer price |

• Government’s publications, reports, databases and studies

• Reports of market research studies and technical publications • Price publications including stock exchange and commodity market quotations • Published accounts and financial statements of the associated enterprises • Agreements and contracts entered into with associated enterprises or with unrelated enterprises • Letters and other correspondence documenting any terms negotiated with the associated enterprise • Documents normally issued in connection with various transactions under the accounting practices followed |

3. What is Safe Harbour and its applicability?

- “Safe Harbour” refers to circumstances under which the Income Tax Authorities shall accept the transfer pricing

declared by the assessee. - Safe Harbour Rules were applicable from AY 2013-14 and the rules were revised from AY 2017-18.

- Eligible transactions to apply under safe harbour rules are:

| International Transactions | Specified Domestic Transactions |

|---|---|

| • Provision of software development services • IT services • Knowledge process outsourcing services • Provision of intragroup loans • Provision of corporate guarantees • Manufacture and export of auto components • Receipt of low-value intragroup services • Provision of contract R&D services relating to software development or generic pharmaceutical drugs |

• Supply of electricity • Transmission of electricity • Wheeling of electricity • Purchase of milk or milk products by a co-operative society from its members |

4. Which forms are required to be filed under transfer pricing?

| Forms | Particulars | Applicability | Timeline |

|---|---|---|---|

| Local file | |||

| 3CEB | Report from the accountant relating to the transaction | Every entity having international or specified domestic transaction | By 31st October of the assessment year |

| – | Transfer Pricing Study Report | Every entity having international transaction where the value exceeds INR 1 crore and eligible specified domestic transactions |

By 31st October of the assessment year |

| Master file | |||

| 3CEAA

(Part A) |

Basic details of the international group and constituent entity by constituent entity | Every constituent entity having international transaction | By 30th November of the assessment year |

| 3CEAA

(Part B) |

Master file information that provides an overview of the international group’s business operations and transfers pricing policies by constituent entity |

Consolidated revenue of international group exceeds INR 500 crores; and

The aggregate value of the international transaction exceeds INR 50 crores, or Aggregate value of international |

By 30th November of the assessment year |

| 3CEAB (Intimation) | Intimation for filing Form 3CEAA by constituent entity | In case, multiple constituent entities resident in India. | By 31st October of the assessment year |

| Country by Country reporting | |||

| 3CEAC | Intimation of details of parent entity/alternate reporting entity not resident in India by Constituent entity |

Consolidated revenue of international group exceeds INR 5,500 crores | By 31st January of the assessment year |

| 3CEAD | Report by a parent entity or the alternate reporting entity resident in India | 12 months from the end of the reporting accounting period | |

| 3CEAE | Intimation on behalf of the international group – no agreement for the exchange of CbCR by Constituent entity |

By 31st January of the assessment year | |

| Safe Harbour rules | |||

| 3CEFA/ 3CEFB | Application for opting for safe harbour in respect of international transaction/ specified domestic transaction |

Every entity having eligible international transaction under safe harbour rules | By 30th November of the assessment year |

5. What are the penalties in case of non-compliance?

| Particulars | Section | Penalty |

|---|---|---|

| Under-reporting of income | 270A(7) | 50% of the tax payable on under-reported income |

| Misreporting of Income | 270A(8) | 200% of the tax payable on misreported income |

| Failure to maintain transfer pricing documents or furnishing incorrect information or document |

271AA(1) | 2% of the value of the transaction |

| Failure to furnish master file(Form 3CEAA, 3CEAB) | 271AA(2) | INR 5,00,000 |

| Failure to furnish the Accountant’s Report(Form 3CEB) | 271BA | INR 1,00,000 |

| Failure to furnish transfer pricing documentation to the Transfer Pricing Officer |

271G | 2% of the value of the transaction |

| Failure to furnish CbCR report (Form 3CEAC, 3CEAD, 3CEAE) |

271GB | Up to 1 month- INR 5,000 per day |

| > 1 month- INR 15,000 per day |

Why choose India Company Incorporation?

At India Company Incorporation, our team provides seamless support

with advisory services. Our experts will assist you in complying with all the applicable laws and frameworks thereafter.

Explore all our tax services and feel free to get in touch with our experts today. To learn more about services, you can

write to us at info@incorpadvisory.in or reach out to us at (+91) 77380 66622.