Introduction

India’s software sector supports the digital economy, driving growth in areas like fintech, ecommerce, manufacturing, and services. With the rise of SaaS, cloud computing, and customized software, understanding GST on software transactions is essential to ensure compliance, correct pricing, and eligibility for input tax credit.

What Is GST on Software Services in India?

The Goods and Services Tax (GST) is a destination-based indirect tax levied on the supply of goods and services. Software is taxable under GST because it qualifies as a “supply,” but its treatment depends on how it is delivered.

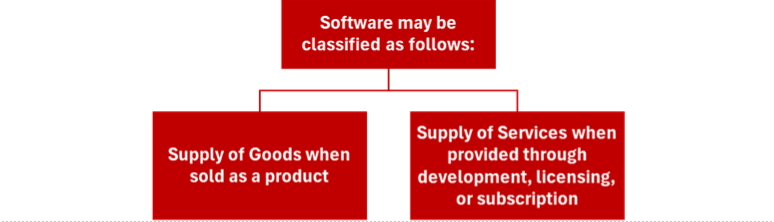

Classification of Software for GST Purposes

The classification of GST software depends mostly on the nature of the transaction and model of licensing.

|

Software is treated as goods when: |

Software is treated as service when: |

|

|

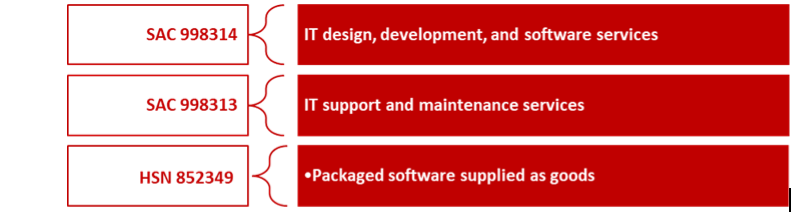

HSN Code for Software Services

What Is an HSN Code?

The Harmonised System of Nomenclature (HSN) is a global standard of nomenclature of goods identification. In the case of services, India makes use of Service Accounting Codes (SAC). Comply with GST and its reporting on returns, it is a requirement to specify the right HSN or SAC on invoices.

Relevant HSN and SAC Codes

There are multiple SAC / HSN codes with respect to supply software as a service or goods depending on the nature of supply. Some commonly used codes are listed below:

GST Portal ‘Search HSN Code’ Link – https://services.gst.gov.in/services/searchhsnsac

The classification should be done based on the nature of the transaction and not the description of the products.

|

GST on software |

GST on Software as a good |

GST on Software as a Service |

| Classification | Packaged or off-the-shelf software classified as goods | Software services, including SaaS subscriptions, are classified as service |

| Rate | 18% | 18% |

|

Example |

Custom Software Development.

Project fee: ₹ 5,00,000 GST @ 18 %: ₹ 90,000 Total invoice value: ₹5,90,000 |

SaaS Subscription

Subscription fee: ₹ 1,00,000 GST @ 18 %: ₹ 18,000 Total invoice value: ₹ 1,18,000 |

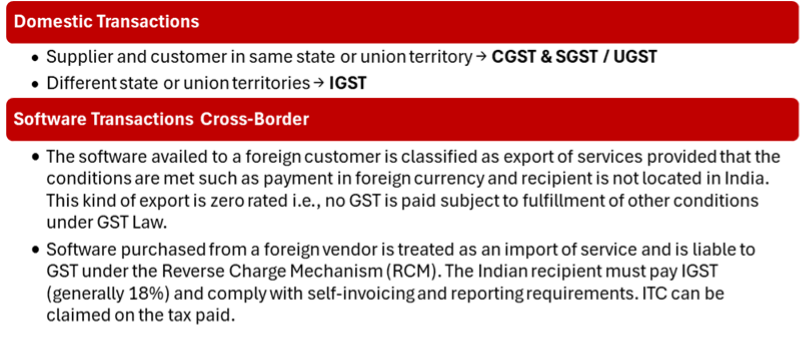

Place of Supply Rules for Software

Place of supply determines whether CGST & SGST / UGST or IGST applies.

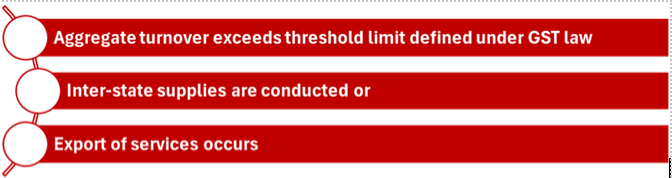

GST Compliance Requirements

The software businesses should be registered when:

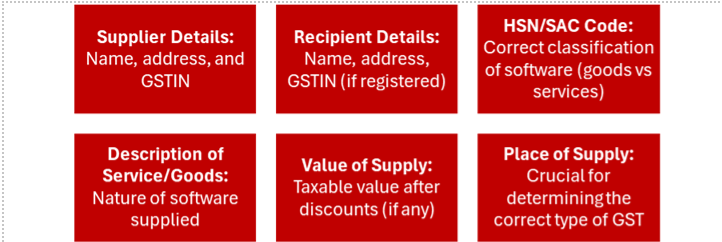

Invoicing Requirements

Filing GST Returns

*Companies under Quarterly Return Monthly Payment (QRMP) are also allowed to submit quarterly returns subject to conditions.

* Software companies are entitled to ITC on GST that has been paid on business inputs like:

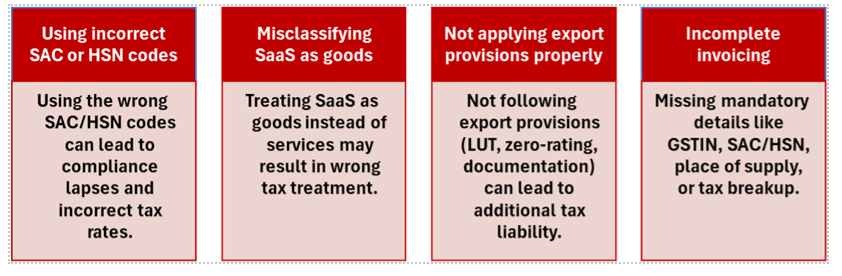

GST Issues Specific to Software Companies

Export of Software Services

Export of service can be done with payment of tax or without payment of tax. If the taxpayer selects without payment of Tax, LUT application needs to be made on GST portal and the LUT number shall mandatorily be mentioned on the Invoice.

Place of Supply in Cross‑Border SaaS

SaaS can be treated as OIDAR service under the IGST Act. The place of supply rules differ for B2B and B2C transactions:

|

B2B (Business to Business) |

B2C (Business to Consumer) |

| Place of supply = Location of recipient. If recipient is outside India → treated as export of service (zero-rated). | Place of supply = Location of recipient (as per OIDAR rules). If service is provided by a foreign supplier to an Indian consumer → GST payable by supplier. |

RCM: If an Indian business receives SaaS from a foreign supplier → GST payable under Reverse Charge Mechanism (RCM).

Withholding Tax vs GST

GST and Withholding Tax (TDS under Income Tax) are separate and independent compliances. GST is a transaction-based tax on the supply of goods or services, while withholding tax is deducted on specified payments and relates to income tax. Payment of GST does not eliminate income tax liability both may apply simultaneously to the same transaction, and businesses must ensure compliance under each law.

Common Mistakes to Avoid

Conclusion

GST on software in India depends on whether it’s treated as a product or a service. Most transactions, especially SaaS and development services are taxed at 18% under SAC 998314. Proper classification, invoicing, and return filing are key for compliance and maximizing input tax credit, while global operations require careful attention to export rules and place-of-supply provisions.

Frequently Asked Questions (FAQs)

1. What is the GST rate on software services?

Most software services and SaaS subscriptions attract 18% GST.

2. Which code applies to SaaS?

SAC 998314 is generally used for SaaS and software development services.

3. Is GST registration required for exporting software?

Yes, exporters must obtain GST registration even though exports are zero-rated.

4. How do I classify custom vs packaged software?

Custom software is treated as a service, while packaged software is treated as goods.

5. What is the difference between SAC and HSN?

HSN is used for goods, while SAC is used for services.