Employee Stock Option Plans (ESOPs) have emerged as a reliable tool for retaining skilled employees, conserving cash resources, boosting productivity, and improving overall profitability across global markets. A growing number of Indian resident employees now receive stock options as part of employee benefit schemes offered by their foreign parent companies. Through these schemes, employees are given the right to acquire shares or other equity interests in the overseas issuing entity once their options vest.

According to the Foreign Exchange Management Act, 1999 (“FEMA”) and its corresponding rules and regulations, an ‘employee benefits scheme’ refers to “any compensation or incentive provided to the directors or employees of an entity that grants them an ownership interest in an overseas entity through an ESOP or any similar scheme.” As a result, this definition covers not only Employee Stock Option Plans (“ESOPs”) but also includes restricted stock unit schemes (RSUs), employee stock purchase schemes (ESPS), and similar arrangements.

What is an ESOP?

An Employee Stock Option Plan (ESOP) serves as a mechanism to reward valuable employees for their contribution. Through this plan, employees receive the right to buy or subscribe to company shares at a later date for a fixed price. This fixed price is typically set below the prevailing market value, and the right to purchase becomes available only after a defined duration called the vesting period. Once the options vest, employees may exercise them, meaning they convert the options into actual shares, which can later be sold to realise potential gains if the company’s valuation increases.

What are Foreign ESOPs?

ESOPs issued by a foreign holding company to the employees of its Indian subsidiary are known as Foreign ESOPs for the Indian employee.

Who is eligible for foreign ESOPs in India?

In India, only employees of the Indian subsidiary, branch, or office of a foreign company are eligible to receive ESOPs granted by the foreign parent. This eligibility framework also aligns with the wider regulatory rules applicable to foreign-owned entities and Company Registration services in india, ensuring that only recognised organisational structures can extend ESOP benefits to employees.

To qualify, the following conditions must typically be met:

- The individual must be a full-time employee or director of the Indian entity

- The foreign company must hold equity, either directly or indirectly, in the Indian entity.

FEMA and Overseas Portfolio Investment (OPI) Rules for Foreign ESOPs

When Indian employees receive ESOPs from a foreign parent company, the transaction falls within the scope of the Foreign Exchange Management Act (FEMA). This regulatory framework is closely connected with the taxation of foreign esops in india, as both compliance and tax treatment operate simultaneously for such equity awards.

From August 2022 onwards, such equity awards are classified as Overseas Portfolio Investments (OPI) under the revised Overseas Investment Rules and Regulations, 2022, issued by the Ministry of Finance and regulated by the Reserve Bank of India (RBI). This framework replaces the earlier treatment under the Liberalised Remittance Scheme (LRS) and directly influences how foreign ESOPS taxation india is interpreted in cross-border employment structures.

Here is what this implies:

1. Uniformity requirement

The foreign parent company must extend ESOPs to Indian employees on the same terms and conditions as those offered to employees in other jurisdictions.

2. Reporting obligations

- If the cost of the ESOP is charged back to the Indian subsidiary, the Indian entity must file Form OPI on a semi-annual basis through its Authorised Dealer (AD) bank.

- These filings must be completed within 60 days from the end of March and September each year.

3. Repatriation rules

If an employee sells shares or receives dividends from the foreign company:

- Where the employee’s holding is less than 10% of the foreign company’s share capital, the proceeds must be repatriated to India or reinvested within 180 days.

- Where the employee’s holding is 10% or more of the foreign company’s share capital, this period is reduced to 90 days.

Note: Repatriation refers to the process of bringing money earned abroad, such as through the sale of shares, back to one’s home country.

Life cycle of ESOP

Below is the flow of an Employee Stock Option Plan (ESOP), from policy execution to employee exercise:

Tax implications in the hands of the employee

Given the multiple stages involved in implementing an ESOP grant, vesting, and exercise it becomes essential to understand the relevant tax provisions to determine how employees are taxed. The tax treatment of foreign ESOPs for Indian employees broadly mirrors the framework applicable to Indian ESOPs under the Income Tax Act, 1961 (the Act).

The taxation of ESOP process occurs in two stages.

At the time of exercise – Tax on perquisite as income from salary;

At the time of sale/transfer – Tax on income from capital gain.

Tax implication at the time of Exercise of ESOP

- Exercise of the options is the first taxable event in the hands of employees when an employee exercises vested options and shares are allotted. The taxable perquisite value is determined under the head of income – “Salary”.

- Taxable perquisite = Difference between the Fair Market Value (FMV) of the shares as on the date of exercise as reduced by the price actually recovered from the employee (i.e. the exercise price).

- This tax is due at exercise even if shares are not sold immediately

- This perquisite is taxed as salary income at the employee’s applicable income tax slab rate. Applicable slab rates under new tax regime for FY 2025-26 are as under:

| Income Slab (₹) | Tax Rate* |

| Up to 4,00,000 | Nil |

| Above 4,00,000 and up to 8,00,000 | 5% |

| Above 8,00,000 and up to 12,00,000 | 10% |

| Above 12,00,000 and up to 16,00,000 | 15% |

| Above 16,00,000 and up to 20,00,000 | 20% |

| Above 20,00,000 and up to 24,00,000 | 25% |

| Above 24,00,000 | 30% |

*Additional surcharge and cess applicable.

Tax Implication at the time of transfer/Sale of ESOPs

- When the employee eventually sells the shares, capital gains tax is levied based on the duration of holding and type of shares.

- Capital gains = Sale price (less) FMV on date of exercise.

- Capital gains are be classified as long-term capital gains or short-term capital gains based on the period of holding of the shares.

| Holding period | Rate (Unlisted shares*) | |

| STCG (Short Term Capital Gain) | Held for less than 24 months from the exercise date. | At the employee’s normal slab rate as given above |

| LTCG (Long Term Capital Gain) | Held for 24 months or more from the exercise date. | at 12.5% for any transfer which takes place on or after 23rd July 2024, as per section 112 of the Act* |

- Foreign ESOPs (whether listed or unlisted) are classified as unlisted equity shares in India.

- The period of holding is calculated from the exercise date to the date of sale. Various case laws1[SP1] have held that shares under ESOPs are allotted only when an employee exercises his ESOP option.

*Indexation benefit has been removed with effect from 23rd July 2024 by Finance Act (No.2) 2024.

Reporting Obligation for Employees for Foreign Assets

Employee Reporting

When an Indian resident employee receives shares in a foreign parent company, they are treated as the owner of those foreign assets. It becomes essential for the employee to report this ownership in their Indian income-tax return (ITR). Under the Income-tax Act, 1961, any individual holding foreign shares or earning income from a foreign company must file an ITR in India, even if their income is below the basic exemption limit.

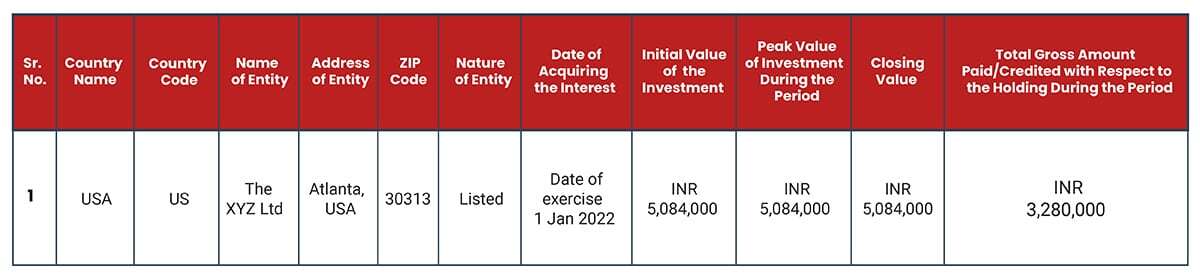

As part of Foreign ESOP reporting, the taxpayer is required to disclose all foreign investments involving overseas entities in Schedule FA of ITR 2 or ITR 3, depending on their income profile. This disclosure includes providing details of shares held in a foreign company in Appendix FA – Details of Foreign Assets. According to the Black Money Act, 2015, failure to report foreign assets, including those arising from a Foreign ESOP, or providing incorrect information in the relevant ITR, may result in a penalty of INR 10 lakhs, irrespective of the value of the assets held outside India.

The below table elaborates an example of how 1000 Foreign ESOP would be declared by Mr. A in the ITR 2, schedule FA.

Timing of reporting foreign ESOPs held by Indian employees:

Avoiding Double Taxation Through DTAA (Double Taxation Avoidance Agreement) and FTC (Foreign Tax Credit)

When Indian employees receive ESOPs from a foreign employer, concerns often arise regarding the possibility of double taxation meaning the same income may be taxed in the employer’s country (such as the U.S.) and again in India, where the employee is a tax resident.

India has Double Tax Avoidance Agreements (DTAAs) with many countries, including the U.S., which are designed to prevent individuals from being taxed twice on identical income. Therefore, it becomes important for both the foreign company and the employee to review the applicable treaty provisions and ensure that all tax-related and reporting requirements in each relevant jurisdiction are fully met.

In the case of cross-border ESOPs, tax liability may arise both in the source country (where the parent company is based) and in India, since Indian residents are taxed on their global income. For example, when ESOP shares are sold, the resulting gain may be taxable under Indian law as well as under the tax rules of the parent company’s country. In certain situations, the foreign employer may also deduct taxes in its own jurisdiction, often through a sell-to-cover arrangement in which a portion of the allotted shares is sold to meet the estimated tax liability overseas.

When such foreign tax is deducted, the employee is eligible to claim a Foreign Tax Credit (FTC) while filing their Indian income-tax return. This credit can be applied to both perquisite income and capital gains.

Foreign Tax Credit is allowed in the year the income is taxed in India, capped at the lower of:

(a) Indian tax on that income or

(b) foreign tax actually paid, with disputed foreign taxes excluded until finally resolved.

To claim FTC, residents must report the foreign income in the return and file Form 67 with details of income and foreign taxes, supported by a certificate/statement from the foreign tax authority, withholding agent, or a self-certified statement with proof of payment.

Overseas Investment Regulations

Foreign ESOPs given to Indian employees are regulated by Foreign Exchange Management (Overseas Investment) Rules, 2022. Under the OI regime, ESOPs in an overseas parent company is generally classified as Overseas Portfolio Investment (OPI) provided the individual’s holding is below 10% of the equity capital and does not confer ‘control’ – this is stated expressly for ESOP/RSU/sweat equity acquired by resident individuals. Foreign ESOPs are not treated as Overseas Direct Investment (ODI)—so long as the employee does not cross the 10% or ‘control’ thresholds.

Many foreign companies rely on advisory firms that offer business set-up services when establishing operations in India, ensuring that their ESOP frameworks remain aligned with FEMA and the OI Rules.

Where employees remit funds abroad for example, to pay an exercise price or to buy shares under an ESOP the payment must route under the Liberalised Remittance Scheme (LRS), which is capped at USD 250,000 per individual per financial year (April–March). Cashless exercises or settlements without outward remittance remain subject to the OI framework even if no LRS is utilised.

Where an overseas parent company grants ESOPs to employees in India, the Indian subsidiary is responsible for coordinating semi-annual reporting in Form OPI through its Authorised Dealer bank. The RBI-prescribed Form OPI must be filed for each half-year period ending 31st March and 30th September. In the case of ESOPs availed by resident individuals, the reporting obligation is expressly cast on the Indian company/branch/office, which is required to furnish a consolidated statement covering all allotments, exercises and transfers during the relevant half-year.

RBI compliance by Indian subsidiaries for foreign ESOPs

Under the FEMA, the Indian subsidiary must file Annual Return (Annexure B) to the Reserve Bank of India (RBI) via the Authorized Dealer (AD) bank in case:

- ESOPs are issued by the foreign holding company to Indian employees.

- Shares are repurchased by the foreign company after being issued under the ESOP scheme.

- The Indian subsidiary mustmaintainappropriate entries in the Register of Directors and Key Managerial Personnel (KMPs) if ESOPs are issued to them.

Given the complexity involved in FEMA filings, Form OPI submissions, and periodic reporting, many Indian subsidiaries depend on specialized business setup & compliance services in India to ensure accurate and timely regulatory adherence.

Accounting standards and cost cross-charging of ESOP costs for foreign ESOP taxation in India

ESOP accounting standards

When a foreign parent company issues ESOPs to employees of its Indian subsidiary, both entities have specific accounting obligations.

The foreign parent is required to follow IFRS 2 and recognise the fair value of the ESOPs as an expense spread across the vesting period.

The Indian subsidiary, which follows Ind-AS 102, must also record this expense, but only in situations where the foreign parent cross-charges the ESOP cost to the Indian entity.

Cost cross-charging

The parent company generally recoups the ESOP-related cost by billing the subsidiary, a mechanism referred to as cross-charging.

The Indian subsidiary is then required to record this amount in its profit and loss statement as an employee benefit expense. This recognition impacts the entity’s taxable income, transfer pricing compliance, and overall profitability.

Key Takeaways and Recommended Action Plan

In India, foreign ESOPs are taxed at two stages: first as a perquisite at the time of exercise, and subsequently as capital gains when the shares are sold.

Equity exercises and share purchases must comply with India’s exchange-control framework, including FEMA and the Liberalised Remittance Scheme (LRS) limits.

Mandatory disclosures apply to both parties: employees must report foreign holdings in their income-tax return (Schedule FA), and employers must file Form OPI through their Authorised Dealer bank.

Action plan for employees

Build the paper trail

Maintain a single folder with grant letters, vesting schedules, exercise confirmations, FMV/valuation evidence, demat/broker statements, and sale proceeds records. Add tax slips/withholding certificates from overseas, Form 67 acknowledgments, and any correspondence with the AD bank.

Plan the cash flow

Anticipate perquisite tax at exercise and any remittance under LRS, factor in forex spreads and timelines with the AD bank.

Disclose without gaps

Report foreign holdings and income in Schedule FA and reflect corresponding income in the ITR; ensure share counts, dates, and amounts reconcile to statements.

Claim treaty relief on time

Where foreign tax is paid and there is double taxation in India as well, file Form 67 and supporting proofs within the prescribed timelines to avail Foreign Tax Credit in India.

Seek expert review

Engage a qualified tax advisor for transaction-level checks (exercise timing, LRS usage, FTC computation) and to align documents before filing.

FAQs

1. How are foreign ESOPs taxed in India?

The way foreign ESOPs are taxed for Indian employees largely mirrors the tax treatment of domestic ESOPs under the Income Tax Act, 1961.

At the time of exercise: The difference between the fair market value (FMV) of the shares on the exercise date and the exercise price is treated as a perquisite (salary income). It is taxed at the employee’s applicable income tax slab, and the employer must deduct TDS.

At the time of sale: When the employee sells the shares, the capital gains are taxed. The gain is calculated as the difference between the sale price and the FMV on the date of exercise.

2. Is ESOP taxed twice in India?

ESOPs generally trigger two taxable events in India.

First, it is taxed as salary (perquisite) when you exercise the options and receive shares.

Then, it is taxed again as capital gains when you sell those shares later.

However, if the employee sells the shares immediately after exercising, the capital gain is typically negligible or non-existent, as the sale price is likely to be very close to, or equal to, the FMV at exercise.

If you are wondering whether foreign ESOPs are taxed twice, the answer is no.

If any foreign tax is paid at either of the above stages, you may be eligible to claim a foreign tax credit under the Double Taxation Avoidance Agreement (DTAA) to prevent double taxation on the same income.

3. When does the taxable event occur for foreign ESOPs in India?

In India, the taxable event for foreign ESOPs typically occurs at two stages.

When the employee exercises the stock option, the difference between the exercise price and the fair market value (FMV) of the shares at the time of exercise is treated as a perquisite and is taxed as salary income.

When the employee sells the shares, any capital gain, which is the difference between the sale price and the FMV at the time of exercise, is taxed as capital gains, either short-term or long-term, depending on the holding period.

4. How are capital gains from foreign ESOP shares handled after the exercise in India?

After an employee exercises their options and later sells the shares, any profit from the sale is treated as a capital gain. The gain is calculated as the difference between the sale price and the market value at the time of exercise. The tax rate depends on the holding period, with different rates for short-term and long-term gains.

5. Is disclosure required for Foreign ESOPs acquired while being a non-resident?

Yes. Although the Foreign ESOPs were acquired when the individual was a non-resident, the individual must disclose these assets under Schedule FA (Foreign Assets) in their Income Tax Return as soon as they become a resident and ordinarily resident in India.

6. Should all employees report Foreign ESOPs received during previous employment?

Yes. All employees are required to disclose foreign assets, including those received during previous employment. Such disclosure is mandatory, regardless of the individual’s current employment status.

7. Can an employee in India file a revised or updated return to comply with the above requirements?

Yes. An employee in India may file a revised return at any time on or before 15 January 2025, for the A.Y. 2024–25, as per CBDT Circular No. 21 of 2024 dated 31 December 2024. In such a revised return, employees in India may comply with the Foreign ESOPs/Assets disclosure reporting requirements.

8. If tax is deducted on ESOPs and included in the ITR, is the penalty levied for non-disclosure of assets in Schedule FA?

Yes. As per the provisions of Sections 42 and 43 of the Black Money Act, failure to disclose or file a return of income despite holding foreign assets, or failure to disclose such foreign assets, is liable to a penalty of INR 10 lakh.

9. Is there a time limit for issuance of notice under the Black Money Act to assess foreign undisclosed income?

No. There is no time limit to issue a notice under the Black Money Act, unlike the Income Tax Act, 1961, where the time limit is three years to reopen the assessment, and six or ten years in certain cases.